30-Year Mortgage Rates as of 5/30/2026: 6.33% to 6.56%

We take an early look at May 2026!

Some Interesting Points:

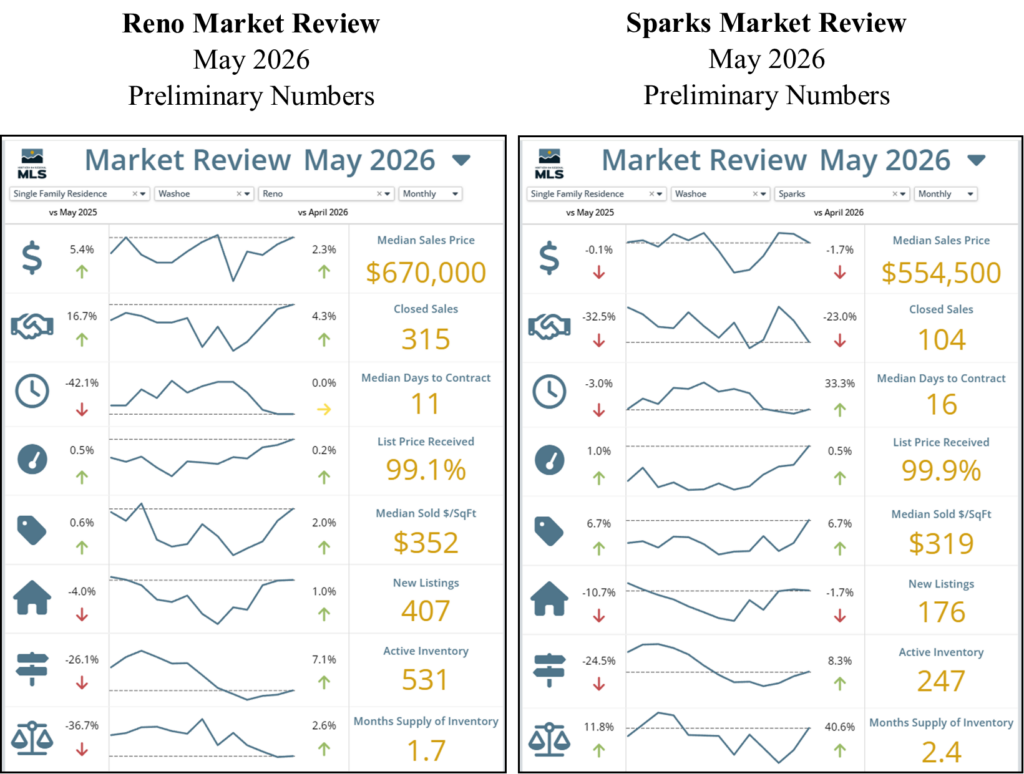

* The initial numbers would indicate that Sparks is falling further behind Reno in the Real Estate Market. I wouldn’t be to firm on these numbers as a lot of transactions can come thru in June that were actually closed and will be reported for May 2026.

30-Year Mortgage Interest Rates continue at about the mid 6’s% and that will continue to put a damper on the Housing Market. At least for buyers. Needless to say, we’re still in a seller’s market:

One of the most frequently asked questions:

- When are the home prices going to come down again? Unfortunately, I give it 99% chance that they will continue to increase a little overall. Maybe 2%-4% per year. In the last 100 years, home prices have substantially decreased at 2 times:

The first was the 1930’s during the great depression and we hope that never happens again! Lots and lots of investors were borrowing money to buy stocks and investments which caused the market to balloon to huge over valuation prices. The market woke up and the everything crashed. Kind of like the 2000 internet bubble, however, the magnitude of the great depression was so huge, it sent the economy into freefall.

The second was 2008, when we had the mortgage meltdown. During that time Reno and Las Vegas saw price declines between 40% and 65%. Why did that happen, well the greedy mortgage lenders (those that consolidated loans into investment opportunities) gave home loans to anyone even if they couldn’t pay their monthly mortgage when the special mortgage rate ended. Eventually, the special mortgage rates ended which caused 2.3 million homes to go into foreclosure. Homes went for sale, in a very small period of time, for about half the original price.

Fast forward to today…Could we have another great depression? Maybe a recession, however, the present indicators of GDP would confirm that’s not likely to happen in the near future and even if it did, we would only see a very small decrease in prices. Probably less than 1% decrease here in Reno/Sparks. There is concern about the price of gas, groceries and cost of living, however, we’re no where near the levels of catastrophe that we saw in the 1930’s. Our leaders have many years of experience and strategies for preventing economic failures, at least we hope they do…lol.

Are there other things that could cause a huge economic downturn/failure? A combination of War, health crises, even a weather disaster could cause home prices to change for a specific geographic area. However, I wouldn’t advise you to make your biggest investment decisions based on events like that. Here’s an interesting look at Reno/Sparks:

Here’s what we do know:

Reno/Sparks housing market is strong with our growing economy. Google and Switch Data Centers are expanding with 15 year construction projects. They employ thousands of construction and high tech workers, from other cities and states. While most aren’t buyers, they do need housing and that pressures rental prices up driving renters to buying. Humm, is there an investor opportunity? Connect with me to discuss further! Tesla just opened their new Semi-Truck manufacturing plant as well as a second battery factory for the 4680 battery.

BTW – the $1 Billion Lyten Lithium-Sulfur Gigafactory that was scheduled to start construction in 2025/2026 has fallen through. They were unable to secure a lease agreement for the facility so Lyten will be looking at other locations.

It’s all good as I just heard that construction has started on 2 Small Data Centers in the North Virginia area close to the Amazon Distribution Center.

Disclaimer – This website contains forward looking statements that are predictions based on data that can and will change as we go forward in time. Today’s economy is filled with changes that happen daily and sometimes hourly. These changes will affect Buyer’s and Seller’s as well as Mortgage Interest Rates and Home Values. You should be cautious in any major purchase and carefully draw your own conclusions on where the market is, where it will go and when.

Conclusions:

If you’re a Buyer – Now is the time to get pre-approved for a mortgage loan. As we shared on our video interview, you need to have Cash, Credit and Income (CC&I). Click here to watch that video. Another great resource, our latest video: How to Improve your Credit Score.

If you’re thinking of Selling – It’s a good idea to have a Realtor complete a Comparative Market Analysis (CMA). Keep in mind there are Automated CMA’s and Manual CMA’s. The difference being a Manual CMA will be more detailed in comparing upgrades. I’d be happy to provide you with either at your request. Click Here to see the Automated CMA for your home and I’ll contact you to discuss further.

After exploring a few of the blog articles on your site, I seriously like your technique of blogging. I book-marked it to my bookmark webpage list and will be checking back soon. Take a look at my website as well and let me know what you think.

Do you mind if I quote a few of your articles as long as I provide credit and sources back to your website? My blog site is in the exact same area of interest as yours and my visitors would really benefit from a lot of the information you provide here.Please let me know if this ok with you. Regards!

Of course, please use any part of my articles!

It’s perfect time to make some plans for the longer term and it’s time to be happy. I’ve read this put up and if I may I wish to suggest you some fascinating issues or suggestions. Perhaps you could write next articles referring to this article. I want to read even more issues approximately it!

Very interesting read, and the videos are so helpful!

Thank you.