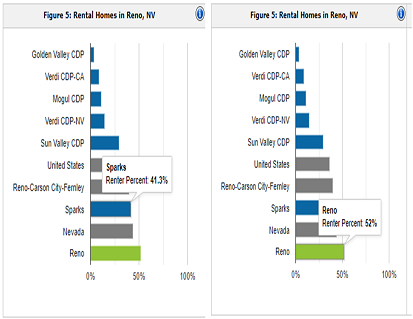

Let’s start with where we are. In 2020, the American Community Survey Census reported that of all homes, condo’s, townhouses, mobile/manufactured homes and apartment units, Reno had 52% as rentals and Sparks at 41.3%. That means that a little less than 50% of all residents in Reno/Sparks are renters.

As you can see in the chart above, that’s higher than the average of the US. So what’s holding back people in Reno from making the move from Renter to Owner? True, some may prefer to rent, others think they can’t afford to buy and even more don’t know where to start? So let’s break it down to some simple steps:

- Get with a loan officer or financial adviser and find out just what you need to do to be ready to buy.

- I know that many people maybe reluctant to share their situation with a stranger, however, this one step is vital and will be eye opening. Based on statistics, most people can be ready to buy in 6-18 months if they have the discipline and decisiveness to stay on plan.

- Set realistic, specific and time bound goals.

- Keep in mind that not everyone can afford a 4-5 bedroom home in South Reno, however, there are some excellent options available in North Reno or other areas. Sometimes, getting into a home that you can afford is the first step to 2 or 3 steps that will lead you to your dream home. You just need to be practical in getting there.

- Create a plan in writing.

- Get your family to understand what you’re doing and why. It will take sacrifice from all members of your family to attain some of these goals and it can and will change the direction of your family.

- Track your progress!

- This is very important, because if you don’t track your progress, you won’t see when you need to adjust. Celebrate successes (milestones) and of course start to plan that purchase as you get closer.

The one thing that is consistent is that if you don’t change what you’re doing as a renter, you probably won’t be a homeowner. Let me share a true story:

I met the Howard (name change) family in January 2021. We went to a loan officer (my preferred loan officer) and they were given some specific challenges:

- Their income is a bit low for a home.

- Mrs. Howard took on a second job as a TSA at the airport

- Mr. Howard worked extra hours to increase his income

- Yes, their income went up and with that their taxes too, but they we’re prepared for that and had the down payment, closing costs and more in hand (about $20+k).

- Their credit score was below 600

- They followed the directions of our loan officer and in January 2022, their score was over 680.

- Their debt-to-income ratio was too high.

- With the extra income, they paid off the car and credit cards. BTW – that helped their credit score too.

- They wanted a home in South Reno, but with the above challenges, the monthly payments for a larger mortgage would be difficult on other parts of their lives. Their daughter recently married and is having their first grandchild (mid-March 2022). They want very much to house their daughter (and husband) & grandchild in their home for the first few years.

- In November 2021, they agreed to look at the North Valleys and we contracted a new home builder for a 4 bedroom, 2.5 bath house for $120k less than what they would have to pay in South Reno.

- On Friday, 02/25/2022 – they closed and received the keys to their brand-new home. BTW – when they got the keys to their house it had already increased in value by $30k.

Now was it hard on the family to overcome those challenges, that’s a huge “YES”.

Will it change the course of their family’s legacy? Probably a bigger “YES”.

Are they determined to help their daughter get into a house, that’s a for sure “YES”.

Buying a home for the first time is one of life’s most difficult tasks and the number of renters in Reno/Sparks is proof of that. If you want to take that first step and prefer some company to help, I will take the first step with you in meeting a loan officer or financial advisor. Julie Millare of Summit Funding heads up our finance team and if you call, text or email Julie or I, we would be happy to set up a first consultation. No cost, no obligation, we just want to help you and your family.