The good news is that you don’t have to save 20% of the home purchase price plus closing costs to purchase a home. There are mortgage loans available that have a 3.5% down payment and if you qualify for a down payment assistance program, you could only need $14k to buy a home. Keep in mind that a smaller down payment will result in a bigger monthly payment and (probably) a higher interest rate. On the other side of the coin, you would surprised how low your monthly payments can get if you increase your down payment.

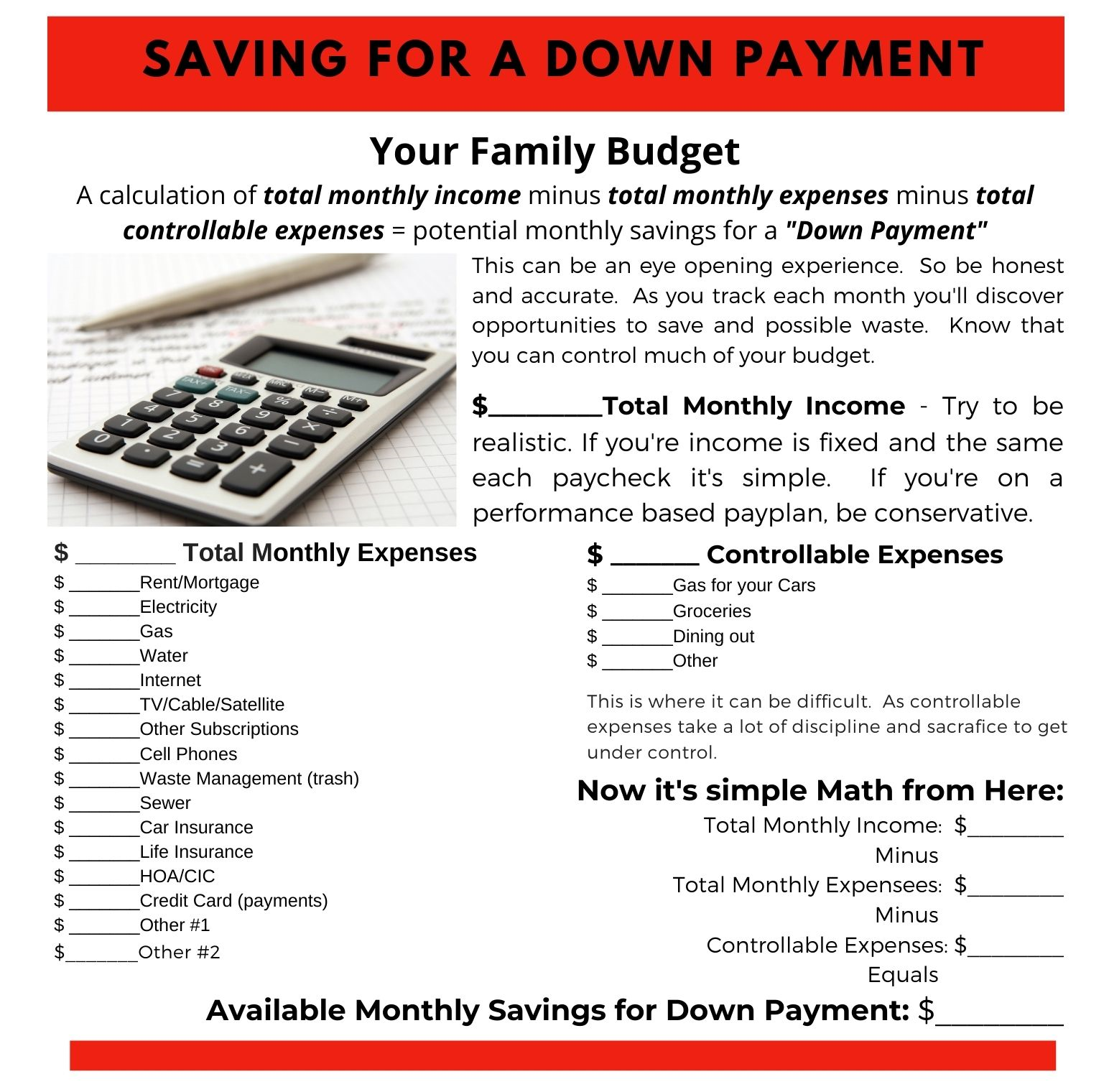

Saving for a down payment could be one of the most difficult task to accomplish. It may take tremendous discipline and sacrifice to save for that down payment. I suggest you take a hard look at your monthly bills and income to calculate just home much you could save each month. Then, you may need to take a hard look at where you can make changes in expenses or income. BTW – you can effect your income by working a part time job (ie – Uber Eats and Doordash are great opportunities that allow you to work when you can and want) or maybe taking those overtime hours (that’s for those of you that work at Tesla/Panasonic or a warehouse jobs). Here’s a basic handy dandy calculator to start your budgeting process:

Hopefully, many of the expenses are blank or zero. You’ll want to also do this for a few months. You’ll see varations each month where you might have repairs on the car, someone has to go to the doctors, or you have a night out. If you record all your expenses and lay them out on a spreadsheet, you may find some interesting expenses that you may adjust in the future.

Huge Tip! – After you’ve completed the budgeting excercise, try setting up a payroll deduction savings plan. Having an amount deducted from your paycheck on a regular basis before you get your paycheck is one of the most popular ways of saving money. Then the task becomes living on what your new paycheck is and not touch your savings account. This really works for a lot of people!

Step #1 – Know exactly how much you’re spending every month and on what! Do that analysis for at least 3 months.

Step #2 – Compare what you’re spending to your income.

Step #3 – If that doesn’t enable you to save for a down payment, take a hard look at spending and your income and where you can make the best adjustments.

Step #4 – Get the family involved (maybe do this early in the process). If you get everyone to buy into the idea of saving to buy a home everyone can help to get that down payment. Yes, teenagers can contibute to the family income and knowing that they will have a home one day to call theirs, can be great motiviation.